Welcome to the answer key for the Economic Skills Lab on interpreting a production possibilities curve. In this lab, we will be exploring the concept of opportunity cost and its relationship to the production possibilities curve. The production possibilities curve is a graphical representation of the different combinations of goods and services an economy can produce with limited resources. By understanding this curve, we can gain insights into the trade-offs and choices faced by individuals, businesses, and nations in allocating resources.

Before we dive into the answer key, let’s quickly recap the basics. The production possibilities curve shows the maximum quantity of one good that can be produced for each possible quantity of another good, given the available resources and technology. It illustrates the concept of scarcity, which is the fundamental economic problem of having unlimited wants and needs but limited resources to satisfy them.

To interpret the production possibilities curve, it is crucial to understand the concept of opportunity cost. Opportunity cost refers to the value of the next best alternative that is foregone when making a choice. It reflects the trade-offs that individuals or societies have to make when allocating scarce resources. On the production possibilities curve, as we move from one point to another, we have to give up some quantity of one good to produce more of the other. This trade-off is the opportunity cost.

Economic Skills Lab Interpreting a Production Possibilities Curve Answer Key

Interpreting a production possibilities curve (PPC) is an essential skill in economics. A PPC is a graphical representation of the different combinations of goods and services that can be produced using given resources and technology. By analyzing a PPC, economists can understand the trade-offs and opportunity costs involved in producing one good over another.

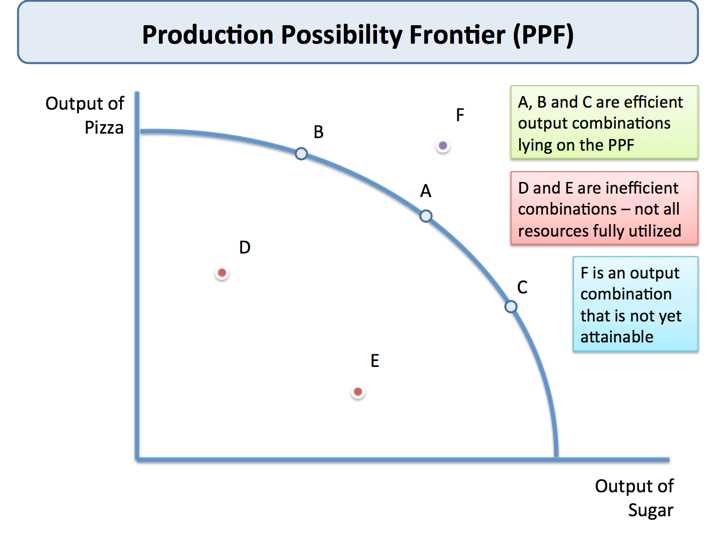

One key aspect of interpreting a PPC is understanding the concept of efficiency. A point on the PPC represents the maximum possible production given the available resources and technology. Points inside the curve indicate inefficient production, while points outside the curve are unattainable with the current resources and technology. Therefore, an economy should strive to operate at a point on the PPC to achieve maximum efficiency.

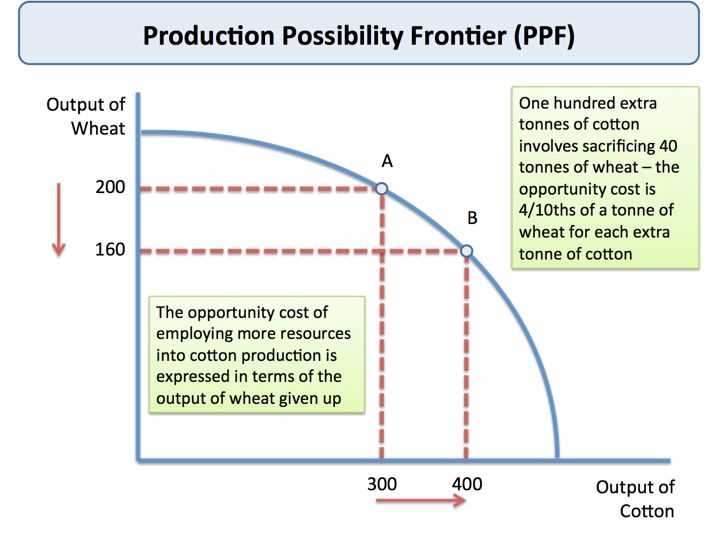

Another important concept is the idea of opportunity cost. As an economy moves from one point on the PPC to another, it must give up some amount of one good to produce more of the other. This concept is illustrated by the shape of the PPC, which is typically bowed outwards. This bow shape indicates that resources are not equally suited to the production of both goods, resulting in increasing opportunity costs as more of one good is produced.

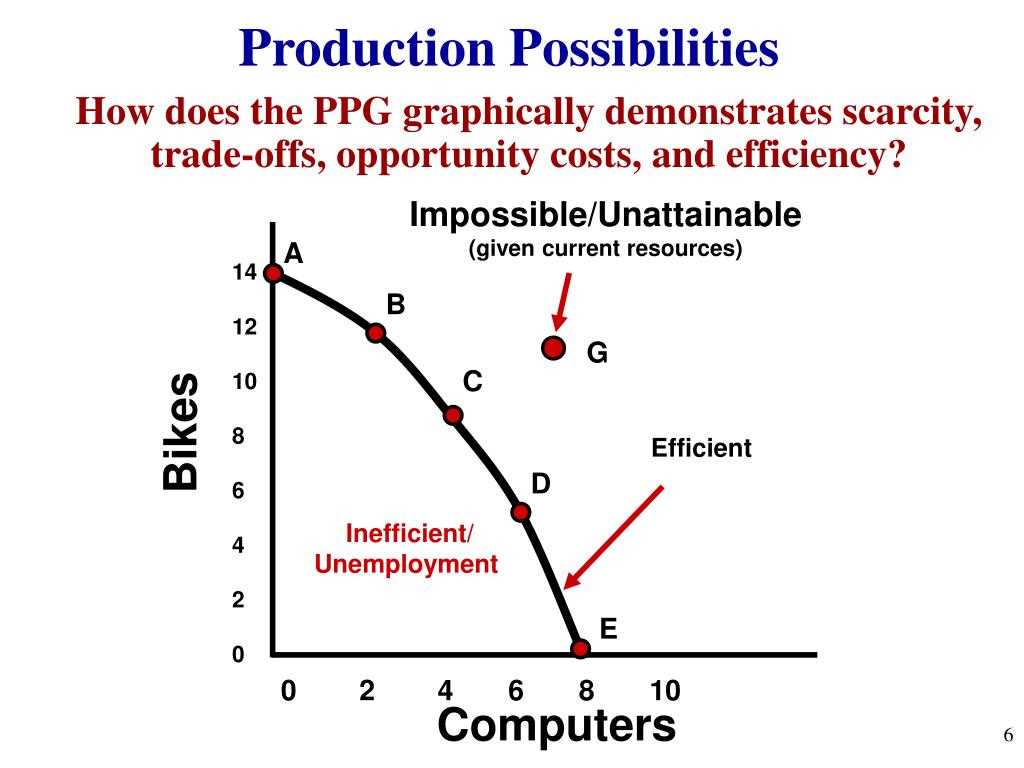

- Point A: At point A, the economy is not using all of its resources to their fullest potential. This indicates inefficiency in production, as more of one good could be produced without sacrificing the production of the other.

- Point B: Point B represents an efficient allocation of resources, as all resources are fully utilized. At this point, the economy is producing a combination of goods that maximizes output given the available resources and technology.

- Point C: Point C is unattainable with the current resources and technology. It represents a combination of goods that exceeds the economy’s production capacity.

In conclusion, interpreting a production possibilities curve requires an understanding of efficiency, opportunity cost, and resource allocation. By analyzing the shape and points on the PPC, economists can gain insights into how an economy utilizes its resources and the trade-offs involved in producing different goods.

What is a Production Possibilities Curve?

A Production Possibilities Curve (PPC), also known as a Production Possibilities Frontier (PPF), is a graphical representation of the various combinations of goods and services that an economy can produce given its resources and technology. It shows the maximum possible output that an economy can achieve when it efficiently uses its resources. The PPC typically displays two goods or services on the x and y axes, and illustrates the trade-offs that must be made when allocating resources between the production of these goods or services.

The PPC is a key tool in economics as it helps illustrate the concept of scarcity and the inherent trade-offs that exist in resource allocation. It shows the different combinations of goods and services that an economy can produce efficiently, given its limited resources. The curve itself is typically bowed outward, illustrating the concept of increasing opportunity cost. As an economy moves along the curve, it must give up increasing amounts of one good in order to produce more of the other.

Overall, the Production Possibilities Curve is a visual representation of the production possibilities available to an economy. By showing the various combinations of goods and services that can be produced efficiently, it helps economists and policymakers analyze the trade-offs and opportunities that exist in resource allocation. The curve is a crucial tool in understanding the limitations and potential of an economy, and is central to the study of economics.

Interpreting Points on a Production Possibilities Curve

The production possibilities curve (PPC) is a graphical representation of the different combinations of goods and services that an economy can produce given its limited resources and technology. Each point on the PPC represents a specific combination of production, and understanding how to interpret these points can provide valuable insights into an economy’s efficiency and trade-offs.

When analyzing points on a PPC, it’s important to consider the concept of opportunity cost. The PPC shows the maximum attainable combination of goods and services, so any movement along the curve represents a trade-off between producing more of one good at the expense of another. In other words, to produce more of good X, a society must give up some production of good Y. This trade-off is reflected in the slope of the PPC, as it measures the rate at which one good can be substituted for another.

Additionally, points inside the PPC indicate an inefficient use of resources, as the economy is not fully utilizing its available resources or technology. These points represent underutilization or unemployment of resources, and indicate a potential for growth and increased production. On the other hand, points outside the PPC are unattainable given the current resources and technology, highlighting the need for improvements or advancements to reach these levels of production.

In conclusion, interpreting points on a production possibilities curve involves understanding opportunity cost, the trade-offs between goods, and the efficiency of resource utilization. By analyzing points on the PPC, economists can assess an economy’s potential for growth and development, and identify areas for improvement or enhancement. The PPC serves as a valuable tool for economic analysis and decision-making in the allocation of resources.

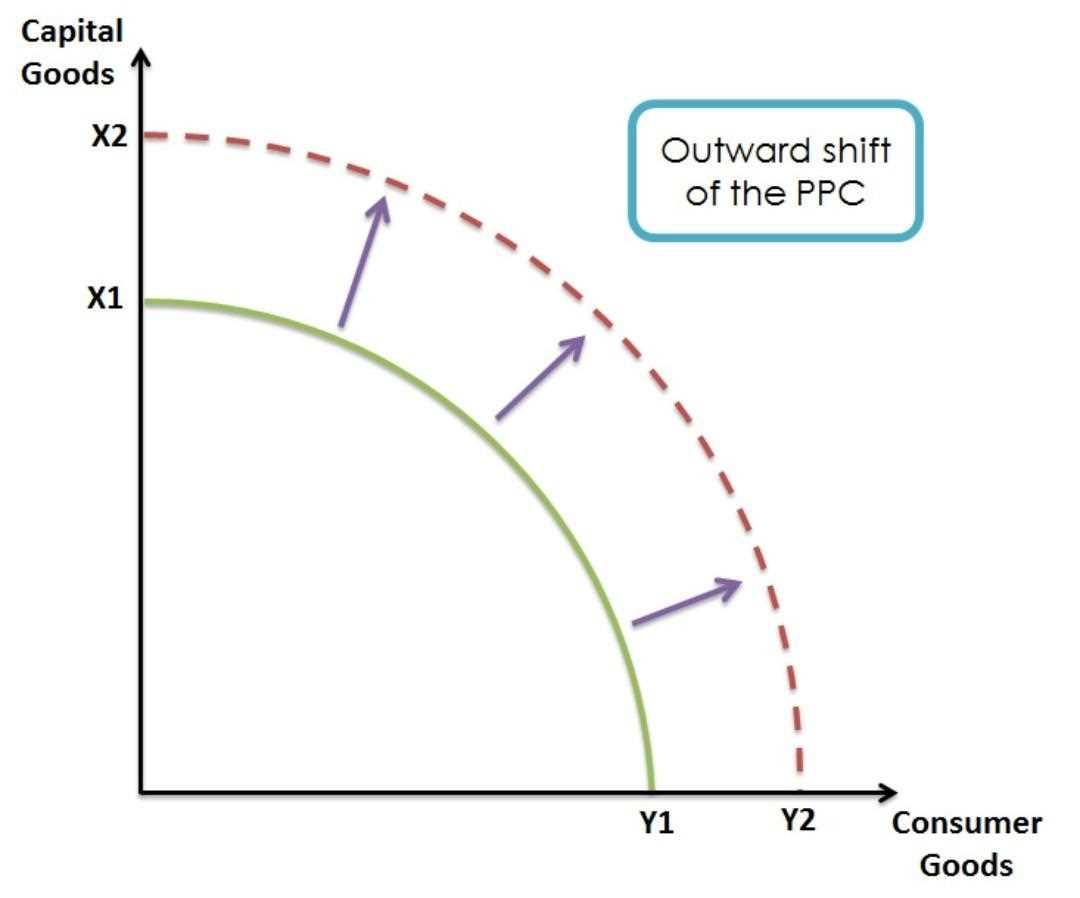

Factors that Shift the Production Possibilities Curve

The production possibilities curve (PPC) represents the different combinations of goods and services that an economy can produce with its available resources and technology. The PPC is a graphical representation of the production capacity of an economy, and it can shift due to various factors.

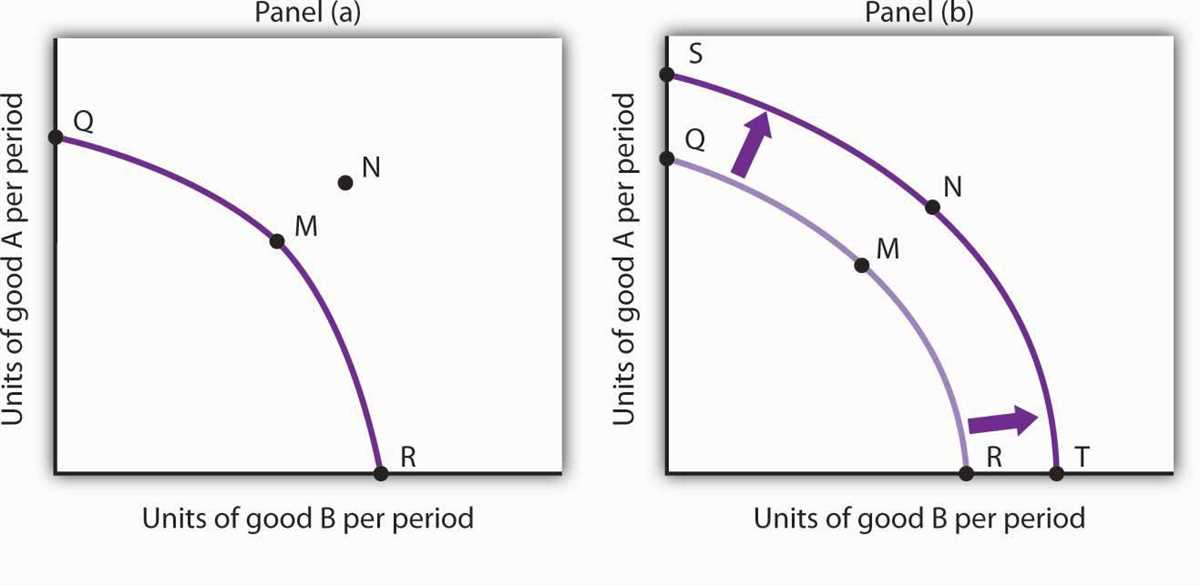

1. Changes in resource availability: The availability of resources, such as natural resources, labor, and capital, can significantly impact the production possibilities of an economy. For example, if a country discovers new oil reserves, it can increase its production capacity for goods and services related to the oil industry, shifting its PPC outward.

2. Technological advancements: Technological advancements can greatly enhance an economy’s production capabilities. Improved technology allows for more efficient use of resources, leading to increased output. For instance, the invention of new machinery or the adoption of better production techniques can shift the PPC outward, enabling the economy to produce more goods and services.

3. Changes in trade: International trade can also affect the production possibilities of an economy. By engaging in trade, a country can import goods and services that it does not produce efficiently, thus freeing up resources to be used in other sectors. This can lead to an increase in the overall production capacity and a shift in the PPC outward.

4. Changes in investment and human capital: Investments in physical capital, such as infrastructure or machinery, can increase an economy’s productive capacity. Similarly, investments in human capital, such as education and training, can enhance the skills and productivity of the workforce. Both of these factors can result in a shift of the PPC outward, allowing for the production of more goods and services.

- Overall, the production possibilities curve is not fixed and can shift due to changes in resource availability, technological advancements, trade, and investments in capital and human capital. These factors play a crucial role in determining an economy’s production capacity and can influence its overall economic growth and development.

Opportunity Cost and the Production Possibilities Curve

The production possibilities curve (PPC) is a graphical representation of the different combinations of two goods or services that a society can produce given its limited resources and current technology. It shows the maximum potential output that can be achieved, assuming full utilization of resources and efficient production. However, the PPC also illustrates the concept of opportunity cost, which is the sacrifice of one good or service in order to produce more of another.

Every point on the PPC represents a trade-off. For example, if a society wants to produce more of one good, such as consumer goods, it must give up some production of another good, such as capital goods. This trade-off is due to the limited resources available in the economy, such as land, labor, and capital. The PPC shows the different combinations of goods that can be produced using these limited resources, and the opportunity cost associated with producing one good over another.

Opportunity cost is the value of the next best alternative that is forgone. It represents what society is giving up in order to produce more of a particular good. For example, if a society decides to increase production of consumer goods, it must give up potential production of capital goods. The opportunity cost of producing more consumer goods is the forgone production of capital goods. The PPC helps to illustrate the concept of opportunity cost by showing the trade-offs between different goods and services.

In conclusion, the production possibilities curve shows the maximum potential output that can be achieved given limited resources and current technology. It also illustrates the concept of opportunity cost, which is the sacrifice of one good or service in order to produce more of another. The PPC helps to visualize the trade-offs and choices that societies face when allocating their limited resources, and highlights the concept of opportunity cost in decision-making.

Efficiency and Inefficiency on the Production Possibilities Curve

The production possibilities curve (PPC) illustrates the maximum potential output combinations of two goods that an economy can produce given its resources and technology. Efficiency and inefficiency can be observed on the PPC, providing valuable information about an economy’s production capabilities.

Efficiency is achieved when an economy operates on the PPC. This means that all available resources are fully utilized to produce a combination of goods that maximizes output. Any point on the PPC represents an efficient allocation of resources, as the economy cannot produce more of one good without sacrificing the production of the other.

On the other hand, inefficiency occurs when an economy operates inside the PPC. In this situation, resources are underutilized, resulting in a production level below the economy’s potential. These points represent missed opportunities, as the economy could produce more of both goods or increase the production of one good without sacrificing the other.

Inefficiency can be caused by various factors, such as unemployment, inadequate technology, or inefficient resource allocation. However, the PPC serves as a visual tool to identify these inefficiencies and guide policymakers in making decisions to improve resource allocation and increase production efficiency.

Applications of the Production Possibilities Curve

The production possibilities curve is a valuable tool in the field of economics that helps to visualize the concept of scarcity and the trade-offs that arise from limited resources. It allows economists to analyze the efficiency of an economy and make predictions about its potential growth and development.

The production possibilities curve can be applied in various ways to provide insights into the economy:

- Resource Allocation: The production possibilities curve can be used to determine the most efficient allocation of resources in an economy. By comparing the levels of production for different goods and services, policymakers can make decisions on how to allocate resources to maximize output.

- Economic Growth: The production possibilities curve can also be used to analyze the factors that contribute to economic growth. A shift outward of the curve indicates an increase in an economy’s productive capacity, which can be attributed to advancements in technology, improvements in infrastructure, or increases in the quantity and quality of resources.

- Opportunity Cost: The production possibilities curve demonstrates the concept of opportunity cost, which refers to the trade-offs a society faces when producing one good over another. The curve shows that as the production of one good increases, there is a decreasing opportunity to produce the other good. This helps policymakers make informed decisions about the allocation of resources and the consequences of their choices.

- Comparative Advantage: The production possibilities curve can also illustrate the concept of comparative advantage, which is the ability of a country to produce a good or service at a lower opportunity cost than another country. By comparing the slopes of the curves for two countries, economists can identify their respective comparative advantages and determine the potential gains from trade.

In conclusion, the production possibilities curve is a powerful tool in economics that allows for the analysis of resource allocation, economic growth, opportunity cost, and comparative advantage. It helps economists and policymakers make informed decisions about the efficient use of resources and the potential for economic development. By understanding the implications of the production possibilities curve, societies can make better choices and strive for more prosperous futures.