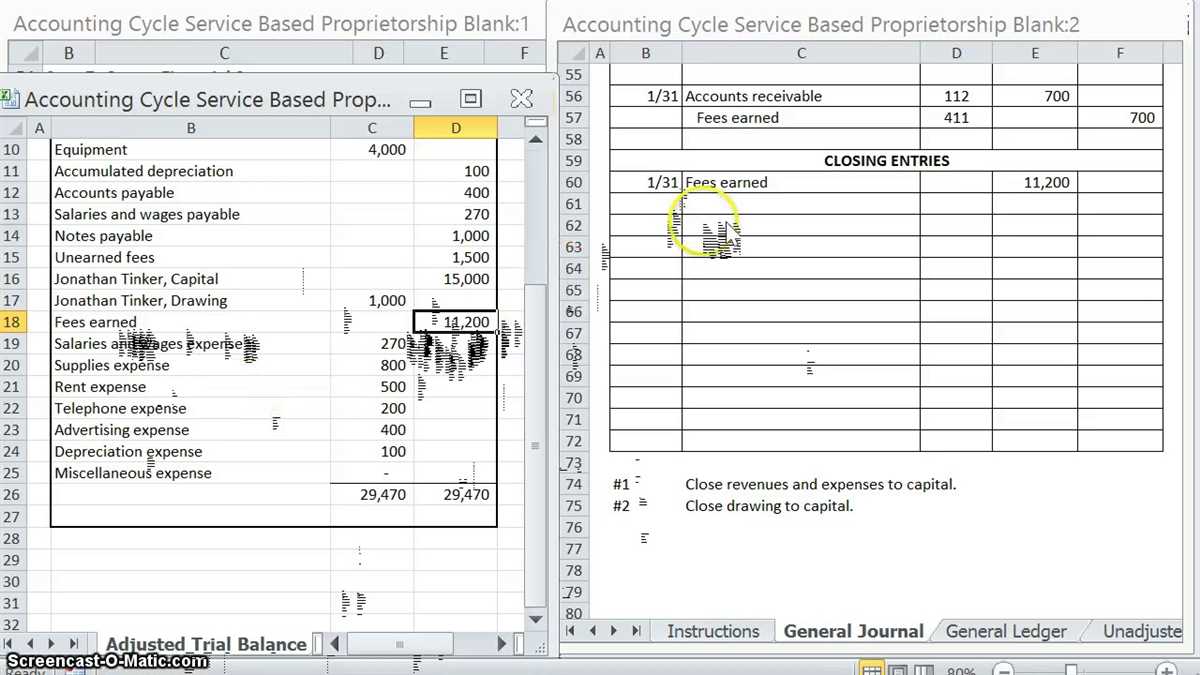

Journalizing closing entries is an important step in the accounting cycle. Closing entries are made at the end of an accounting period to transfer the balances of temporary accounts, such as revenues and expenses, to permanent accounts, such as retained earnings.

Problem 10-6 requires the journalizing of closing entries, which involves analyzing the trial balance and determining the appropriate closing entries for the period. The answers to this problem will provide a comprehensive understanding of the process and the impact it has on the financial statements.

By correctly journalizing closing entries, businesses ensure that their financial statements accurately reflect the financial position and performance for the period. These entries also reset the temporary accounts to zero, preparing them for the next accounting period.

In conclusion, understanding how to journalize closing entries is crucial for maintaining accurate and reliable financial records. Problem 10-6 provides an opportunity to practice this skill and gain a deeper understanding of the impact closing entries have on the overall accounting process.

What are Closing Entries and Why are They Important?

Closing entries are the final entries made in a company’s accounting records at the end of an accounting period. These entries are used to transfer the balances of temporary accounts, such as revenue, expenses, and dividends, to the permanent accounts on the balance sheet. Closing entries are essential because they help reset the temporary accounts to zero and prepare the books for the next accounting period.

Temporary accounts, also known as income statement accounts, are used to track revenues, expenses, and withdrawals over a specific period of time. These accounts are not carried forward to the next accounting period, as their balances serve to measure the company’s performance during that period. By closing these accounts, the company starts with a clean slate in the new accounting period.

The process of closing entries typically involves the following steps:

- Identifying and listing all the temporary accounts to be closed, including revenue accounts, expense accounts, and withdrawal accounts.

- Transferring the balances of these accounts to the retained earnings or owner’s equity account.

- Preparing an income summary account to temporarily hold the revenue and expense balances before transferring them to the retained earnings or owner’s equity account.

- Closing the income summary account by transferring its balance to the retained earnings or owner’s equity account.

- Recording the closing entry for the dividends account, if applicable.

- Verifying that the temporary accounts now have zero balances and ensuring that the permanent accounts are updated accordingly.

Closing entries play a crucial role in the accounting cycle as they ensure the accuracy and integrity of the financial statements. They enable the company to report the revenues, expenses, and owner’s equity for a specific period, providing valuable information for decision-making and financial analysis. Additionally, closing entries help maintain the transparency and accountability of the company’s financial records by separating transactions between different accounting periods.

Understanding the Purpose of Closing Entries in Accounting

In accounting, closing entries are essential to accurately measure a company’s financial performance and prepare financial statements for a specific period. These entries are made at the end of the accounting period to close temporary accounts and transfer their balances to permanent accounts. The primary purpose of closing entries is to reset the temporary accounts, such as revenue, expenses, and dividends, to zero, so that the next accounting period starts with accurate and up-to-date financial information.

Temporary accounts:

Temporary accounts, also known as nominal accounts, are used to record transactions and events that are specific to a specific accounting period. These accounts include revenue accounts, expense accounts, and dividend accounts. Revenue accounts record income generated from the company’s primary activities, while expense accounts track the costs incurred to generate that income. Dividend accounts, on the other hand, record the distribution of profits to the company’s shareholders.

Closing process:

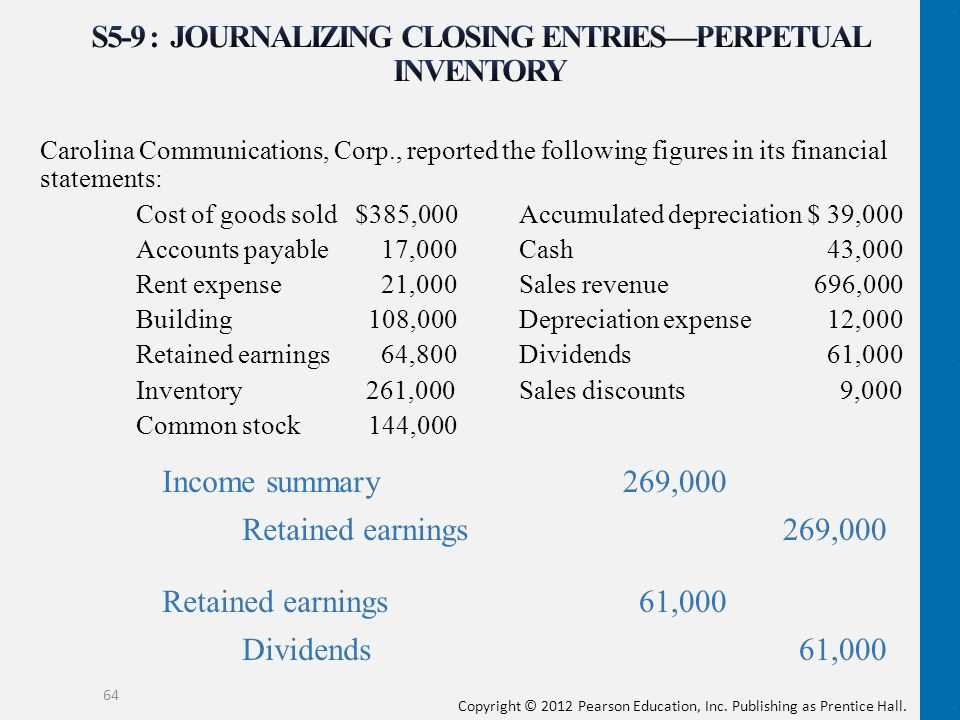

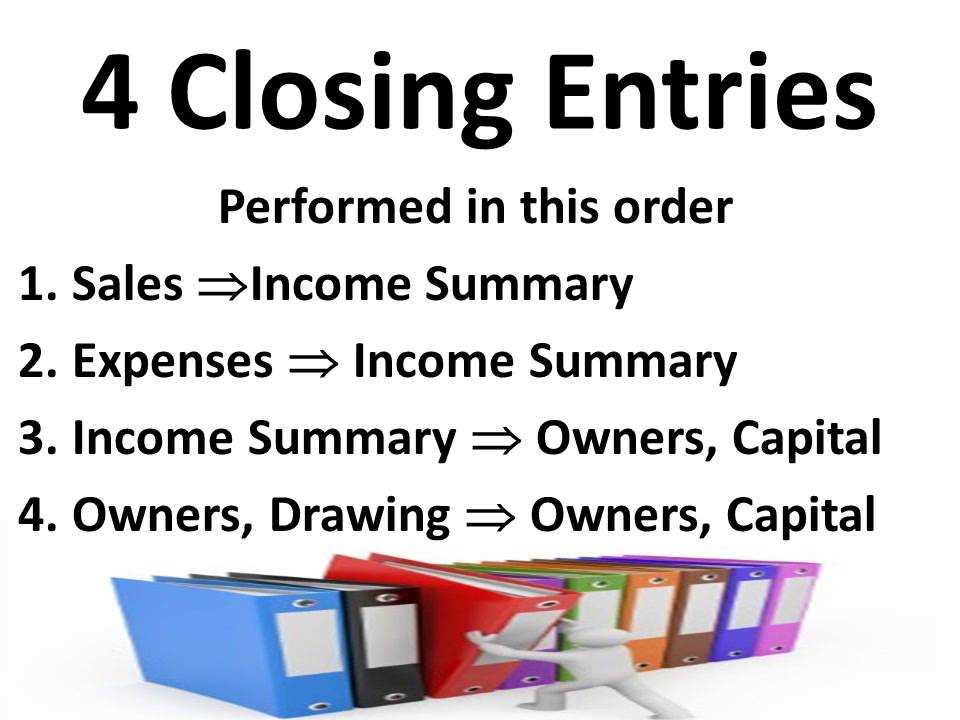

The closing process involves four steps: closing revenue, closing expense, closing income summary, and closing dividends. First, the revenue accounts are closed by transferring their balances to the income summary account. This step helps determine the net income or loss for the period. Next, the expense accounts are closed by transferring their balances to the income summary account. The income summary account then reflects the overall net income or loss for the period.

Finally, the balance in the income summary account is transferred to the retained earnings account, and the dividends account is closed by transferring its balance to the retained earnings account. These closing entries bring the temporary accounts to zero and update the retained earnings account with the net income or loss and the dividends distributed during the period. As a result, the company’s financial statements present accurate information about its financial performance and position.

Importance of closing entries:

The purpose of closing entries is to ensure that each accounting period starts with zero balances in the temporary accounts. This allows for the accurate recording of new transactions and provides a clean slate for measuring financial performance. Additionally, closing entries help summarize the company’s revenue, expenses, and net income or loss for the period, enabling management and stakeholders to make informed decisions based on reliable financial information.

In summary, closing entries play a crucial role in the accounting cycle by closing temporary accounts, updating the retained earnings account, and providing accurate financial information for the next accounting period. By understanding the purpose of closing entries, accountants can ensure the reliability and accuracy of financial statements and assist in sound decision-making for the company.

The Steps Involved in Journalizing Closing Entries

Closing entries are an important part of the accounting process as they help to reset the revenue and expense accounts to zero and transfer their balances to the retained earnings account. Journalizing closing entries involves several steps that must be followed accurately for the financial records to be correct.

Step 1: Identify the accounts to be closed. Before closing entries can be journalized, it is necessary to determine which accounts need to be closed. This typically includes revenue accounts, expense accounts, and any other temporary accounts that have accumulated balances throughout the accounting period.

Step 2: Determine the closing entries. Once the accounts to be closed have been identified, the next step is to determine the specific closing entries that need to be recorded. For revenue accounts, the entry will debit the revenue account and credit the income summary account, while for expense accounts, the entry will debit the income summary account and credit the expense account. The balances of these temporary accounts will ultimately be transferred to the retained earnings account.

Step 3: Journalize the closing entries. After determining the closing entries, the next step is to journalize them in the general journal. This involves recording the debit and credit entries for each account being closed, as well as the income summary account. The amounts used in the entries should match the balances in each account to be closed.

Step 4: Post the closing entries to the general ledger. Once the closing entries have been recorded in the general journal, they must be posted to the general ledger. This involves transferring the debit and credit entries from the journal to the appropriate accounts in the ledger. Each entry should be posted to the corresponding account with the correct amount.

Step 5: Calculate and record the new balance for the Retained Earnings account. After posting the closing entries, the final step is to calculate and record the new balance for the Retained Earnings account. This can be done by adding the net income or subtracting the net loss for the period, along with any additional adjustments such as dividends. The closing entries should have transferred the balance of each temporary account to the Retained Earnings account.

Following these steps in journalizing closing entries ensures that the financial records accurately reflect the revenues, expenses, and retained earnings for the accounting period. It helps reset the temporary accounts for the next period and provides a clear picture of the company’s financial performance.

Common Problems and Challenges in Journalizing Closing Entries

Journalizing closing entries is a crucial step in the accounting process that helps ensure the accuracy of financial statements. However, there are several common problems and challenges that can arise during this process.

1. Incorrect Account Balances: One of the primary challenges in journalizing closing entries is ensuring that the account balances are accurate. Errors in posting transactions or miscalculations can lead to incorrect closing entries, which can ultimately impact the accuracy of financial statements.

2. Missing Entries or Transactions: Another common problem is the omission of necessary closing entries or transactions. Failing to record all necessary adjustments can result in incomplete or inaccurate financial statements, which can have serious consequences for a business.

3. Improper Classification: It is essential to correctly classify accounts when journalizing closing entries. Misclassifying accounts can lead to errors in the closing process and may ultimately result in inaccurate financial statements.

4. Failure to Account for Adjustments: Closing entries are meant to account for temporary accounts, such as revenue and expense accounts. Failing to include all necessary adjustments can result in the carryover of these balances into the next accounting period, leading to inaccurate financial statements.

5. Lack of Understanding or Knowledge: Journalizing closing entries requires a solid understanding of accounting principles and practices. For individuals who lack knowledge or experience in this area, it can be challenging to accurately journalize closing entries and ensure the integrity of financial statements.

Overcoming these challenges requires careful attention to detail, double-checking calculations, and implementing internal controls to ensure the accuracy of account balances and the proper classification of accounts. It may also be beneficial to seek assistance from a professional accountant or use reliable accounting software to streamline the closing entry process.

Strategies to Ensure Accuracy and Efficiency in Journalizing Closing Entries

Journalizing closing entries is an important step in the accounting process as it helps summarize the financial activities of a business for a specific accounting period. To ensure accuracy and efficiency in journalizing closing entries, several strategies can be implemented:

1. Review the trial balance:

Prior to journalizing closing entries, it is crucial to review the trial balance to ensure that all accounts are properly recorded and balanced. Any errors or discrepancies should be identified and corrected before proceeding with the closing entries.

2. Follow the correct closing entry procedure:

It is essential to follow the correct closing entry procedure to ensure accuracy in journalizing closing entries. This involves closing the temporary income and expense accounts to the income summary account, transferring the balance of the income summary account to the retained earnings account, and closing the dividend account to retained earnings (if applicable).

3. Use standardized templates or software:

Using standardized templates or accounting software can contribute to the accuracy and efficiency of journalizing closing entries. These tools provide a structured format for entering the necessary information and perform calculations automatically, reducing the risk of manual errors.

4. Reconcile the closing entries with supporting documentation:

After journalizing the closing entries, it is important to reconcile them with supporting documentation, such as financial statements and transaction records. This verification step helps ensure that the closing entries accurately reflect the financial position of the business.

5. Perform periodic reviews and audits:

To maintain accuracy in journalizing closing entries, periodic reviews and audits should be conducted. These reviews can identify any errors or discrepancies and allow for timely corrective actions to be taken. Regular audits provide an added layer of assurance that the closing entries are accurate and in compliance with accounting standards.

By implementing these strategies, businesses can ensure that their journalizing closing entries are accurate, efficient, and in accordance with accounting principles. This, in turn, provides reliable financial information for decision-making and reporting purposes.

Frequently Asked Questions about Journalizing Closing Entries

In accounting, closing entries are made at the end of an accounting period to transfer the balances of temporary accounts to permanent accounts. This process helps reset the accounts for the next period and ensures accurate financial reporting. Here are some frequently asked questions about journalizing closing entries:

1. What are temporary accounts and permanent accounts?

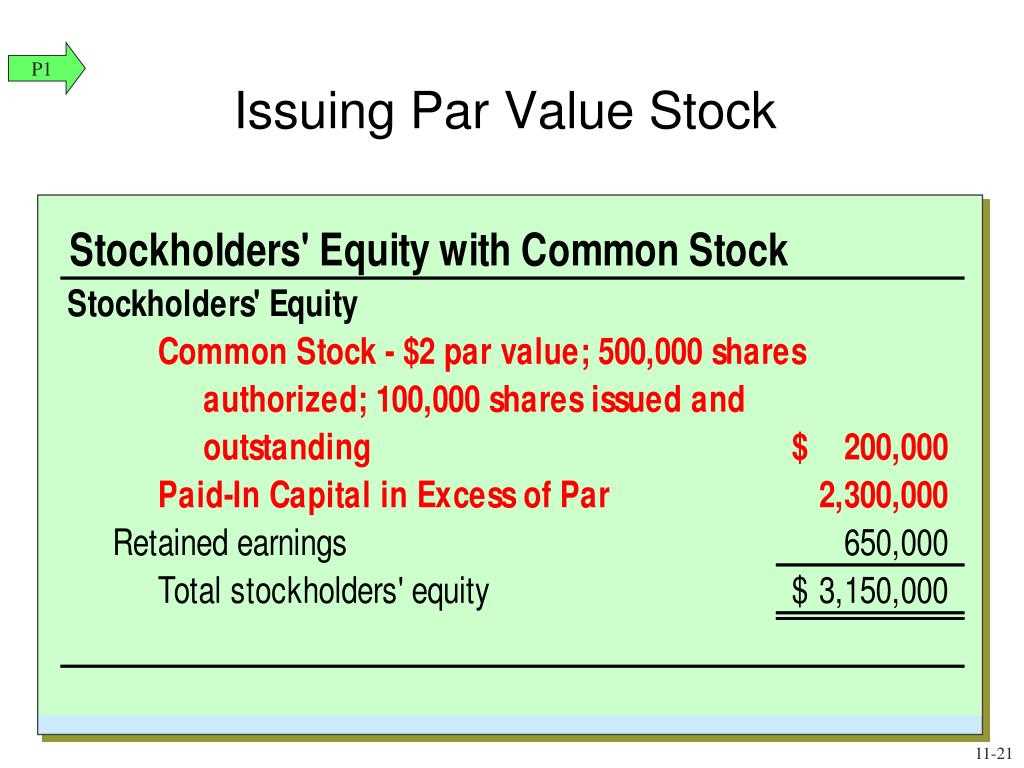

Temporary accounts are accounts that track the revenue, expenses, gains, and losses incurred during a specific accounting period. These accounts are closed at the end of each period and their balances are transferred to permanent accounts. Permanent accounts, on the other hand, are accounts that track assets, liabilities, and equity, and their balances carry over from one accounting period to the next.

2. What is the purpose of journalizing closing entries?

The purpose of journalizing closing entries is to reset the temporary accounts to zero and transfer their balances to permanent accounts. By doing so, the company can start the next accounting period with accurate balances in each account and ensure the financial statements reflect only the relevant information for the period.

3. How are closing entries journalized?

Closing entries are journalized by debiting the balances of revenue accounts and crediting the balances of expense accounts to transfer their amounts to the income summary account. The income summary account is then debited or credited to transfer the net income or net loss to the retained earnings account. Finally, the balances of the temporary accounts are closed by transferring them to the retained earnings account through journal entries.

4. Can closing entries be reversed?

Closing entries are typically not reversed because their purpose is to reset the temporary accounts for the next period. Reversing closing entries would result in inaccurate balances and distort the financial statements. However, if an error is identified in the closing entries, adjusting entries can be made in the subsequent period to correct the mistake.

5. What happens if closing entries are not made?

If closing entries are not made, the balances of the temporary accounts from the previous period will be carried over to the next period. This can lead to inaccurate financial reporting as the balances may not reflect the actual revenue, expenses, gains, and losses incurred during the specific period. It is essential to make closing entries to ensure the accuracy of the financial statements.

Overall, journalizing closing entries is an important step in the accounting process to reset temporary accounts, transfer balances, and ensure accurate financial reporting for each period.

Key Takeaways on Journalizing Closing Entries in Accounting

The process of journalizing closing entries in accounting is a crucial step in the financial accounting cycle. It is the final step before preparing financial statements, and it helps ensure accurate reporting of a company’s financial performance.

1. Purpose of Closing Entries:

- Closing entries are necessary to transfer temporary accounts’ balances to the retained earnings account.

- They help reset the temporary accounts to zero for the new accounting period.

- Closing entries summarize the revenue, expense, and withdrawal activities for the period.

2. Types of Closing Entries:

- Revenue accounts: These accounts are credited to close them.

- Expense accounts: These accounts are debited to close them.

- Withdrawal account: This account is debited to close it.

- Retained earnings account: This account is credited to capture the net income or loss of the period.

3. Accounting Process for Closing Entries:

- Identify the temporary accounts that need to be closed.

- Journalize the closing entries in the general journal.

- Post the closing entries to the corresponding ledger accounts.

- Calculate the net income or loss by subtracting the total expenses from the total revenues.

- Record the net income or loss in the retained earnings account.

4. Importance of Accuracy:

It is crucial to ensure the accuracy of the closing entries to prevent any errors in the financial statements. Properly journalizing and posting the closing entries will result in precise financial reporting and provide a clear picture of the company’s financial position.

5. Support for Decision Making:

By journalizing closing entries accurately, stakeholders can make informed decisions based on reliable financial information. The closing entries help summarize the financial activities for the period, enabling stakeholders to evaluate the company’s performance and plan for the future.

Overall, the process of journalizing closing entries is integral to maintaining accurate financial records and producing reliable financial statements. It ensures the clear separation of different accounting periods and provides valuable information for decision-making purposes.